Updated July 27, 2023

Bond Pricing Formula (Table of Contents)

Bond Pricing Formula

Bond pricing is the formula used to calculate the prices of the bond being sold in the primary or secondary market.

Where

- n = Period which takes values from 0 to the nth period till the cash flows ending period

- Cn = Coupon payment in the nth period

- YTM = interest rate or required yield

- P = Par Value of the bond

Examples of Bond Pricing Formula (With Excel Template)

Let’s take an example to understand the calculation of Bond Pricing in a better manner.

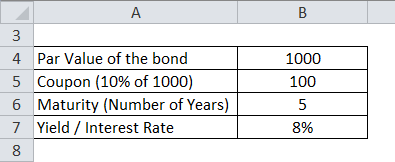

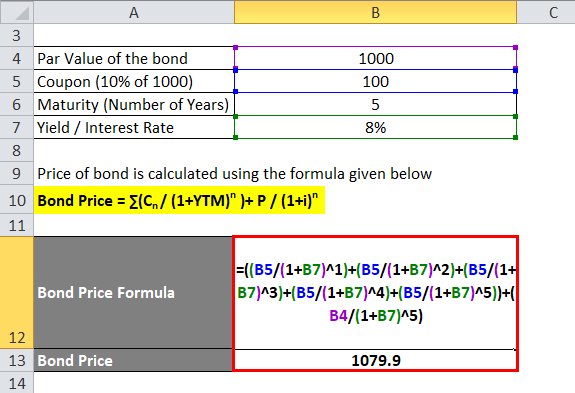

Bond Pricing Formula – Example #1

Let’s calculate the price of a bond which has a par value of Rs 1000 and coupon payment is 10% and the yield is 8%. The maturity of a bond is 5 years.

Price of bond is calculated using the formula given below

Bond Price = ∑(Cn / (1+YTM)n )+ P / (1+i)n

- Bond Price = 100 / (1.08) + 100 / (1.08) ^2 + 100 / (1.08) ^3 + 100 / (1.08) ^4 + 100 / (1.08) ^5 + 1000 / (1.08) ^ 5

- Bond Price = 92.6 + 85.7 + 79.4 + 73.5 + 68.02 + 680.58

- Bond Price = Rs 1079.9

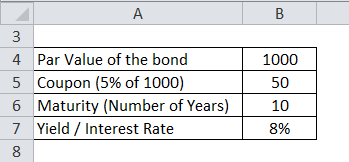

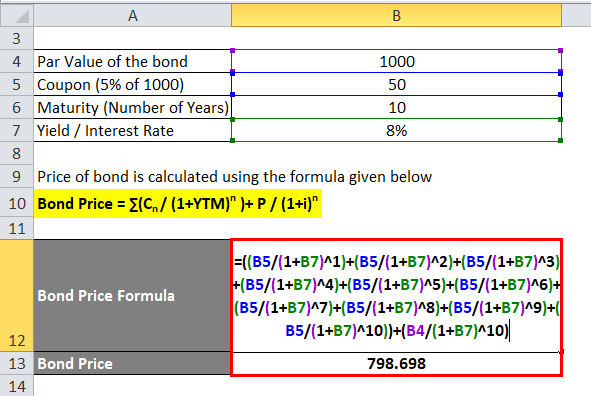

Bond Pricing Formula – Example #2

Let’s calculate the price of a Reliance corporate bond which has a par value of Rs 1000 and coupon payment is 5% and yield is 8%. The maturity of the bond is 10 years

Price of bond is calculated using the formula given below

Bond Price = ∑(Cn / (1+YTM)n )+ P / (1+i)n

- Bond Price = 50 / (1.08) + 50 / (1.08) ^2 + 50 / (1.08) ^3 + 50 / (1.08) ^4 + 50 / (1.08) ^5 + 50 / (1.08) ^6 + 50 / (1.08) ^7 + 50 / (1.08) ^8 + 50 / (1.08) ^9 + 50 / (1.08) ^10 + 1000 / (1.08) ^ 10

- Bond Price = 46.3 + 42.87 + 39.69 + 36.75 + 34.03 + 31.51 + 29.17 + 27.01 + 25.01 + 23.16 + 463.19

- Bond Price = Rs 798.698

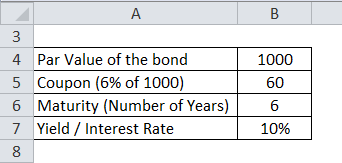

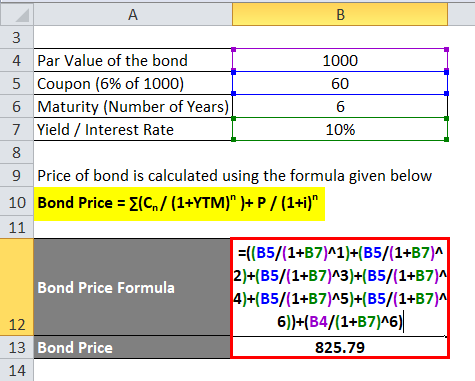

Bond Pricing Formula – Example #3

Let’s calculate the price of a Tata Corp. corporate bond which has a par value of Rs 1000 and coupon payment is 6% and yield is 10%. The maturity of the bond is 6 years

Price of bond is calculated using the formula given below

Bond Price = ∑(Cn / (1+YTM)n )+ P / (1+i)n

- Bond Price = 60 / (1.1) + 60 / (1.1) ^2 + 60 / (1.1) ^3 + 60 / (1.1) ^4 + 60 / (1.1) ^5 + 60 / (1.1) ^6 + 1000 / (1.1) ^ 6

- Bond Price = 54.55 + 49.59 + 45.08 + 40.98 + 37.26 + 33.87 + 564.47

- Bond Price = Rs 825.79

Explanation of Bond Pricing Formula

As can be seen from the Bond Pricing formula, there are 4 factors that can affect the bond prices. The factors are illustrated below: –

- Par Value or Face Value (P) – This is the actual money that is being borrowed by the lender or purchaser of bonds. Generally, it is 100 or 1000 per nay bond. The principal amount borrowed by the lender is the number of bonds purchased multiplied by the par value.

- Tenor or Years of Maturity (n) – This describes the number of years that it takes for any bond to mature or when the issuer of bonds will return the par value to the purchaser of bonds.

- Yield to Maturity (YTM) – This can be described as the rate of return that the purchaser of a bond will get if the investor holds the bond till its maturity. Also, this could be the prevailing interest rate to calculate the current market price of the bond.

- Coupon Rate (C) – This is the periodic payment, usually half-yearly or yearly, given to the purchaser of the bonds as interest payments for purchasing the bonds from the issuer.

The bond prices are then calculated using the concept of Time Value of Money wherein each coupon payment and subsequently, the principal payment is discounted to their present value based on the prevailing interest rates.

Relevance and Uses of Bond Pricing Formula

The bond prices are affected by the above mentioned factors and some of the points to remember are: –

- Any bond which has a higher coupon payment will have a higher price

- Any bond which has a higher par value will have a higher price

- Any bond which has a higher years to maturity will have a higher price

- Any bond which has a higher yield to maturity will have a lower price

These mentioned factors affect the bonds in the primary market. There are other factors which affect the bond prices in the secondary market. They are: –

- Credit rating or creditworthiness of the issuer of bonds

- Liquidity of the secondary market for bonds

- Time for the next payment of bonds

Bonds issued by government or corporates are rated by rating agencies like S&P, Moody’s, etc. based on the creditworthiness of issuing firm. The ratings vary from AAA (highest credit rating) to D (junk bonds) and based on the rating the yield to maturity varies. The higher rated bonds will offer a lower yield to maturity. Bonds which are traded a lot and will have a higher price than bonds that are rarely traded. Time for next payment is used for coupon payments which use the dirty pricing theory for bonds. The dirty price of a bond is coupon payment plus accrued interest over the period. As the coupon disbursal date gets closer, bondholder has to wait lesser time to receive his payment hence one needs to provide added incentive to make that bondholder sell his bond which drives up demand and hence increases the prices of bonds.

Conclusion

Bond pricing formula depends on factors such as a coupon, yield to maturity, par value and tenor. These factors are used to calculate the price of the bond in the primary market. In the secondary market, other factors come into play such as creditworthiness of issuing firm, liquidity and time for next coupon payments.

Recommended Articles

This has been a guide to Bond Pricing formula. Here we discuss How to Calculate Bond Pricing along with practical examples. We also provide downloadable excel template. You may also look at the following articles to learn more –